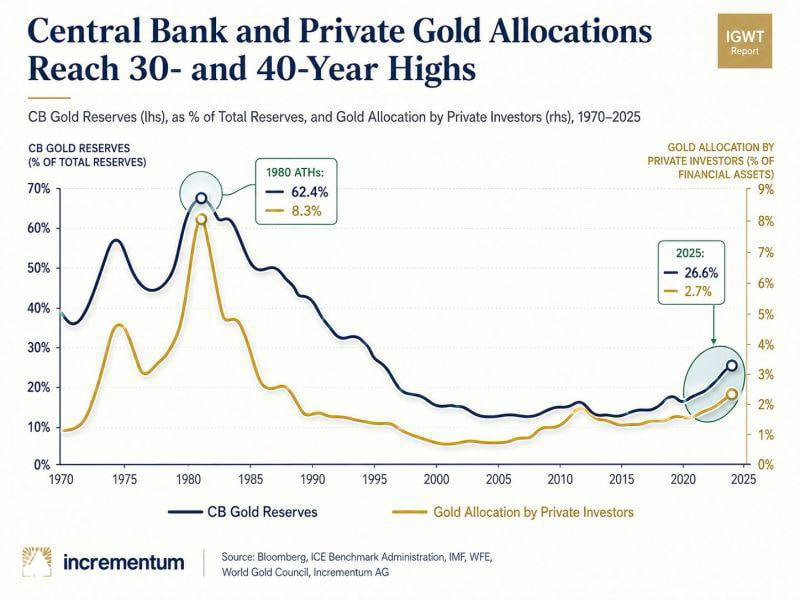

Private investors hold just 2.7% of financial assets in gold.

In 1980 it was 8.3%. Central banks sit at 26.6% versus 62.4% back then.

The historical comparison suggests that the current bull market is being driven more by official-sector demand than by retail participation. While central banks have been accumulating gold at one of the fastest rates in decades, private investors remain significantly underallocated relative to previous market peaks, indicating that the investment cycle may still be in its earlier stages.

Even a modest increase in portfolio allocations could translate into significant incremental demand given the limited annual supply of physical gold.

Given that private investor allocations remain well below historical peaks despite record central bank purchases, maintaining a strategic allocation of 5–10% to gold may enhance portfolio resilience against inflation, geopolitical uncertainty, and financial market stress.